Black-Litterman Portfolio Optimization MCP Server

Enables AI agents to perform Black-Litterman portfolio optimization with investor views, backtesting, and asset analysis, generating dashboards for visualization.

README

Black-Litterman Portfolio Optimization MCP Server

![]()

Black-Litterman portfolio optimization MCP server for AI agents

Works with Claude Desktop, Windsurf IDE, Google ADK, and any MCP-compatible AI

Features

- Portfolio Optimization - Black-Litterman model with sensitivity analysis

- Investor Views - Absolute/relative views with confidence levels

- Backtesting - Strategy comparison, drawdown analysis, timeseries

- Asset Analysis - Correlation matrix, VaR, per-asset statistics

- Dashboard Generation - Visualization hints for AI-generated charts

- Multiple Assets - S&P 500, NASDAQ 100, ETF, Crypto, custom data

Quick Start

Option 1: Smithery (Easiest - No Installation!) 🌟

Install via Smithery in one command:

npx @smithery/cli install @irresi/bl-view-mcp --client claude

Or visit smithery.ai/server/@irresi/bl-view-mcp and click:

- "Add to Claude Desktop" - One-click setup

- "Add to ChatGPT" - Direct integration

- "Run" - Test in browser instantly

No Python/uv installation needed! Smithery hosts the server for you.

Option 2: Local Installation (uvx)

For offline use or development:

Step 1: Find uvx path

Run in terminal:

which uvx

# Example output: /Users/USERNAME/.local/bin/uvx

If uvx is not installed:

curl -LsSf https://astral.sh/uv/install.sh | sh

Step 2: Configure Claude Desktop

Config file location:

- macOS:

~/Library/Application Support/Claude/claude_desktop_config.json - Windows:

%APPDATA%\Claude\claude_desktop_config.json

File content (replace with your uvx path):

{

"mcpServers": {

"black-litterman": {

"command": "/Users/USERNAME/.local/bin/uvx",

"args": ["black-litterman-mcp"]

}

}

}

Step 3: Restart Claude Desktop

Cmd+Q (macOS) or fully quit and restart

Usage

Ask Claude:

"Optimize a portfolio with AAPL, MSFT, GOOGL. I think AAPL will return 10%."

First run: S&P 500 data auto-downloads (~30 seconds)

Tip: Want charts or dashboards? Just ask: "Show me a dashboard with the results" or "Create a visualization of the portfolio weights"

Example Use Cases

Try these prompts with Claude:

Note: Default period is 1 year for all tools. All returns are annualized - when you say "outperform by 40%", it means 40% annual return expectation.

Basic Optimization + Visualization

Optimize a portfolio with AAPL, MSFT, GOOGL, NVDA. I am confident that NVDA will outperform others by 40%. Show me a dashboard.

Backtesting with Benchmark

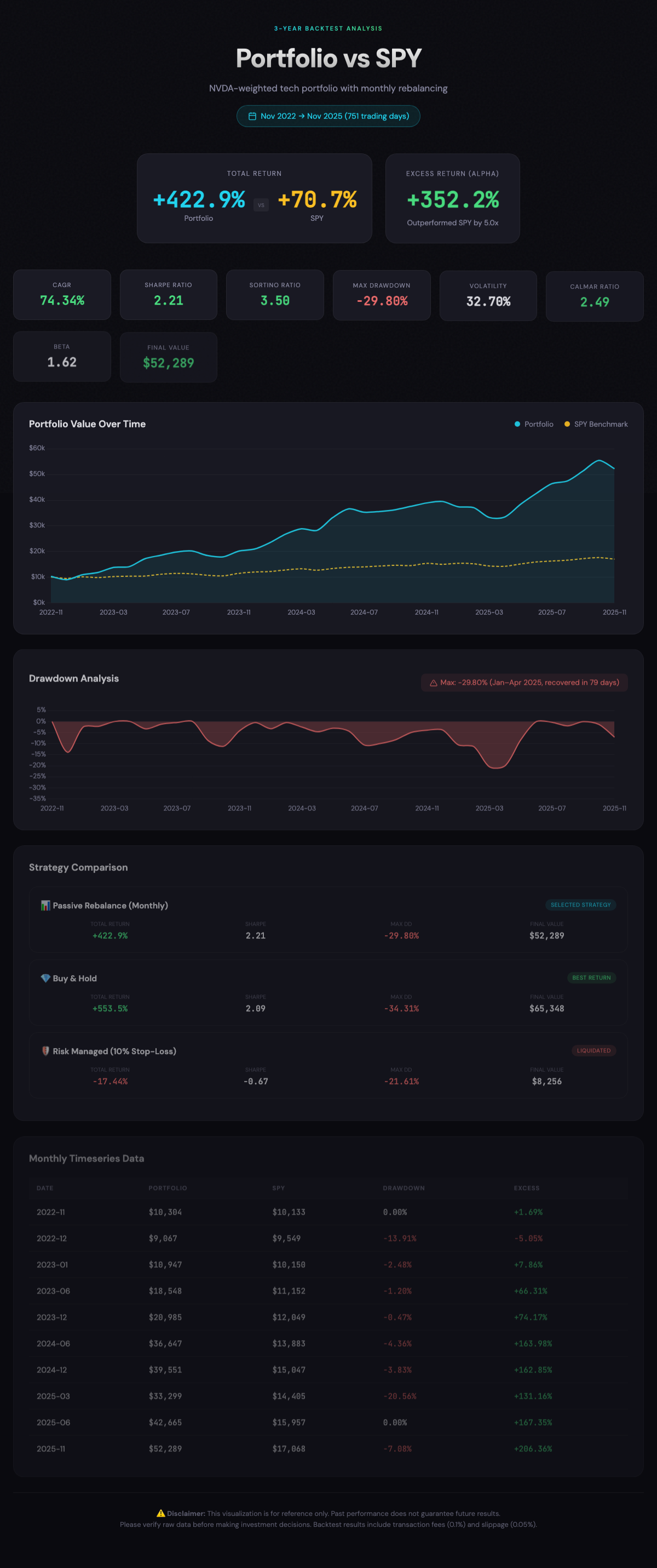

Backtest the above optimized portfolio for 3 years and compare with SPY.

Strategy Comparison

Compare buy_and_hold, passive_rebalance, and risk_managed strategies for this portfolio.

Correlation Analysis

Analyze the correlation between NVDA, AMD, and INTC.

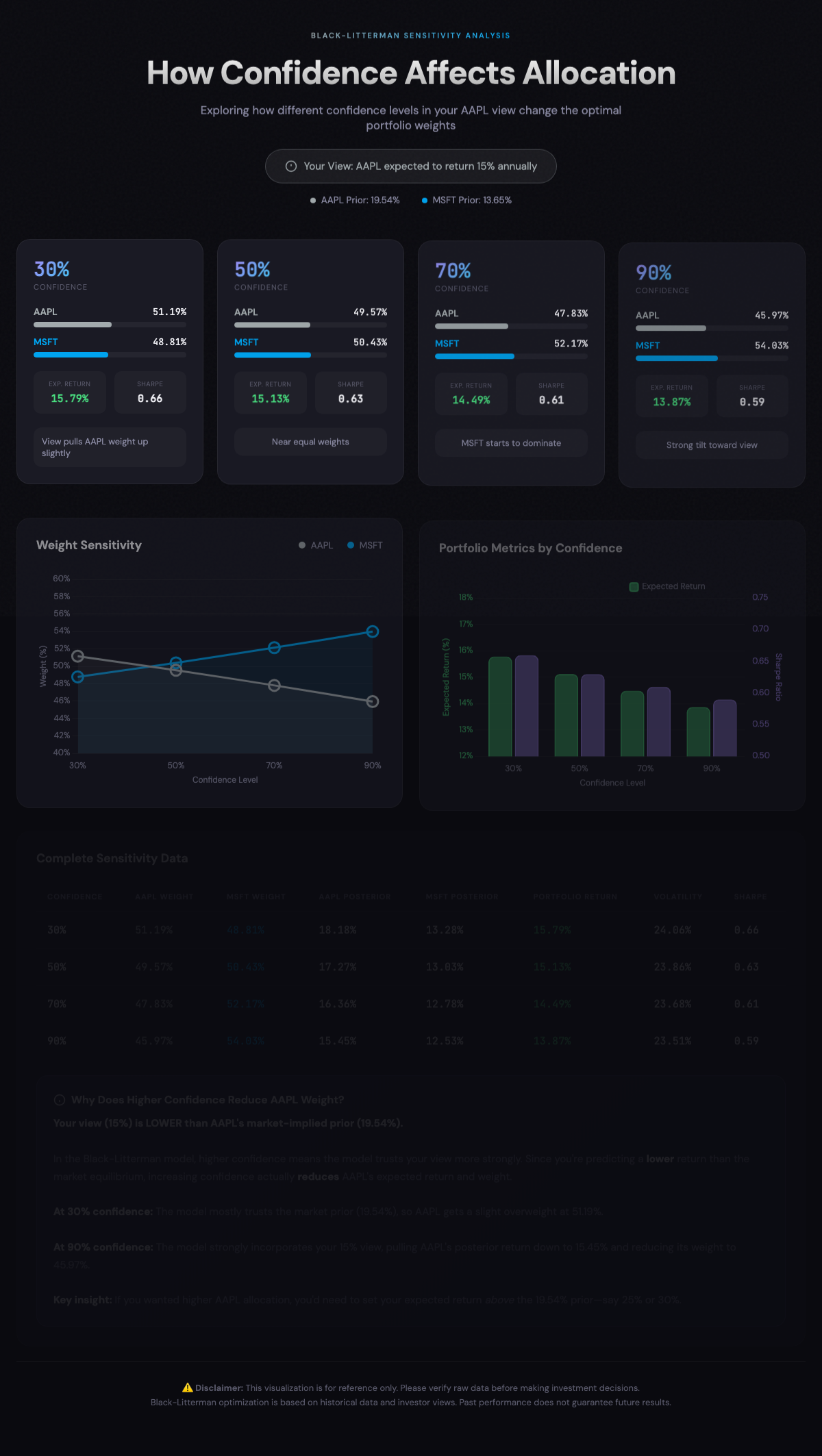

Sensitivity Analysis

Create a portfolio with AAPL and MSFT. I expect AAPL to return 15%. Run sensitivity analysis with confidence levels 0.3, 0.5, 0.7, 0.9.

Demo Dashboards

Generated using the example prompts above with Claude Desktop:

<ins>Click images</ins> to view interactive HTML dashboards:

| Optimization | Backtest | Strategy |

|---|---|---|

|

|

|

| Correlation | Sensitivity |

|---|---|

|

|

Other Installation Methods

pip (Python Package)

Install directly from PyPI:

pip install black-litterman-mcp

Then configure your MCP client to run:

black-litterman-mcp # or bl-view-mcp, bl-mcp

Requires Python 3.11+. Data auto-downloads on first use.

Windsurf IDE

.windsurf/mcp_config.json:

{

"mcpServers": {

"black-litterman": {

"command": "/Users/USERNAME/.local/bin/uvx",

"args": ["black-litterman-mcp"]

}

}

}

From Source (Developers)

git clone https://github.com/irresi/bl-view-mcp.git

cd bl-view-mcp

make install

make download-data # S&P 500 data

make test-simple

Docker

docker build -t bl-mcp .

docker run -p 5000:5000 -v $(pwd)/data:/app/data bl-mcp

Google ADK Web UI

Test with Google ADK (Agent Development Kit):

# Terminal 1: Start MCP HTTP server

make server-http # localhost:5000

# Terminal 2: Start ADK Web UI

make web-ui # localhost:8000

Open http://localhost:8000 in browser

Requires

make install(includes google-adk dependency)

Supported Datasets

| Dataset | Tickers | Description |

|---|---|---|

snp500 |

~500 | S&P 500 constituents (default) |

nasdaq100 |

~100 | NASDAQ 100 constituents |

etf |

~130 | Popular ETFs |

crypto |

~100 | Cryptocurrencies |

custom |

- | User-uploaded data |

PyPI install: S&P 500 data auto-downloads on first run

Source install: Download additional datasets manually

make download-data # S&P 500 (default)

make download-nasdaq100 # NASDAQ 100

make download-etf # ETF

make download-crypto # Crypto

MCP Tools

optimize_portfolio_bl

Calculate optimal portfolio weights using Black-Litterman model.

optimize_portfolio_bl(

tickers=["AAPL", "MSFT", "GOOGL"],

period="1Y",

views={"P": [{"AAPL": 1}], "Q": [0.10]}, # AAPL expected 10% return

confidence=0.7,

investment_style="balanced" # aggressive / balanced / conservative

)

Views examples:

# Absolute view: "AAPL will return 10%"

views = {"P": [{"AAPL": 1}], "Q": [0.10]}

# Relative view: "NVDA will outperform AAPL by 20%"

views = {"P": [{"NVDA": 1, "AAPL": -1}], "Q": [0.20]}

VaR Warning: When predicted returns exceed 40%, EGARCH-based VaR analysis is automatically included in the warnings field.

backtest_portfolio

Validate portfolio strategy with historical data.

backtest_portfolio(

tickers=["AAPL", "MSFT", "GOOGL"],

weights={"AAPL": 0.4, "MSFT": 0.35, "GOOGL": 0.25},

period="3Y",

strategy="passive_rebalance", # buy_and_hold / passive_rebalance / risk_managed

benchmark="SPY"

)

get_asset_stats

Get asset statistics including VaR, correlation matrix, and covariance matrix.

get_asset_stats(

tickers=["AAPL", "MSFT", "GOOGL"],

period="1Y",

include_var=True # Set False for faster response (skips EGARCH VaR)

)

# Returns: assets (price, return, volatility, sharpe, var_95, percentile_95),

# correlation_matrix, covariance_matrix

upload_price_data

Upload external data (international stocks, custom assets, etc.).

# Direct upload (small data)

upload_price_data(

ticker="005930.KS", # Samsung Electronics

prices=[

{"date": "2024-01-02", "close": 78000.0},

{"date": "2024-01-03", "close": 78500.0},

...

],

source="custom"

)

# Or load from file (large data)

upload_price_data(

ticker="CUSTOM_INDEX",

file_path="/path/to/data.csv",

date_column="Date",

close_column="Close"

)

list_available_tickers

Query available tickers.

list_available_tickers(search="AAPL") # Search

list_available_tickers(dataset="snp500") # S&P 500 only

list_available_tickers(dataset="custom") # Custom data

Documentation

| Document | Description |

|---|---|

| docs/TESTING.md | Testing guide |

| docs/ARCHITECTURE.md | Technical architecture |

Tech Stack

- MCP Server: FastMCP

- Optimization: PyPortfolioOpt

- Risk Model: arch (EGARCH)

- Data: yfinance, ccxt (crypto)

License

MIT License - LICENSE

Troubleshooting

"spawn uvx ENOENT" / "uv binary not found"

Claude Desktop may not recognize system PATH. Use absolute path:

which uvx

# Use the output path in config

"Data file not found"

Source install:

make download-data

PyPI install: Auto-downloads on first run (~30 seconds).

"uv: command not found"

curl -LsSf https://astral.sh/uv/install.sh | sh

Need more help?

Recommended Servers

playwright-mcp

A Model Context Protocol server that enables LLMs to interact with web pages through structured accessibility snapshots without requiring vision models or screenshots.

Magic Component Platform (MCP)

An AI-powered tool that generates modern UI components from natural language descriptions, integrating with popular IDEs to streamline UI development workflow.

Audiense Insights MCP Server

Enables interaction with Audiense Insights accounts via the Model Context Protocol, facilitating the extraction and analysis of marketing insights and audience data including demographics, behavior, and influencer engagement.

VeyraX MCP

Single MCP tool to connect all your favorite tools: Gmail, Calendar and 40 more.

graphlit-mcp-server

The Model Context Protocol (MCP) Server enables integration between MCP clients and the Graphlit service. Ingest anything from Slack to Gmail to podcast feeds, in addition to web crawling, into a Graphlit project - and then retrieve relevant contents from the MCP client.

Kagi MCP Server

An MCP server that integrates Kagi search capabilities with Claude AI, enabling Claude to perform real-time web searches when answering questions that require up-to-date information.

E2B

Using MCP to run code via e2b.

Neon Database

MCP server for interacting with Neon Management API and databases

Qdrant Server

This repository is an example of how to create a MCP server for Qdrant, a vector search engine.

Exa Search

A Model Context Protocol (MCP) server lets AI assistants like Claude use the Exa AI Search API for web searches. This setup allows AI models to get real-time web information in a safe and controlled way.